In the competitive landscape of Los Angeles real estate in 2026, the definition of a “Top Producer” has shifted. It is no longer enough to be a master of local aesthetics or a high-level negotiator. Today, the most successful agents in LA have transformed into Risk Mitigation Consultants.

Following the devastating wildfires of early 2025… the Insurance Exodus in Southern California has reached a breaking point, forcing a total evolution in how we close escrow(PreventionWeb). With major carriers like State Farm, Farmers, and Allstate further scaling back their presence, insurance is no longer a “check-the-box” item—it is the #1 reason deals die in escrow.

Surviving the Insurance Exodus: Why 13% of California Deals Failed

For realtors, the “Insurance Exodus” is a direct threat to their livelihood. Data indicates that 13% of California Realtors reported at least one sale falling through specifically because the buyer could not secure homeowners insurance—a rate that nearly doubled in a single year (Real Estate News).

In Los Angeles, this crisis is amplified by high property values, where a single rejected insurance application can blow a buyer’s Debt-to-Income (DTI) ratio and disqualify them from a loan entirely.

Understanding the Risk Factor: The Agent’s New Liability

In 2026, the risk factor for a real estate agent isn’t just a lost commission; it’s a legal liability. California law imposes a strict fiduciary duty on agents to disclose “material facts” that affect the value or desirability of a property (Wolff Law).

Why “Insurability” is Now a Material Fact

If an agent sells a home in a high-risk zone (like the Hollywood Hills or Pacific Palisades) without discussing the difficulty of obtaining insurance, they open themselves up to Errors and Omissions (E&O) lawsuits. Buyers who find themselves stuck with a “California FAIR Plan” bill that costs 4x the market average may claim the agent failed to disclose the true “cost of ownership.”

The Risk Factors Include:

- DTI Blowouts: High premiums can push a buyer’s monthly debt above the lender’s limit, killing the loan at the 11th hour.

- Property Value Compression: Homes that are uninsurable or prohibitively expensive to cover are seeing price drops of 10% or more as the buyer pool shrinks to “cash-only” investors.

- Non-Disclosure Lawsuits: Failing to warn a client about “Zone Zero” vegetation requirements or insurer retreats in specific ZIP codes is now seen as professional negligence.

3 Strategic Pillars to Protect Your Commission in 2026

To beat the Insurance Exodus, agents must move insurance from a closing afterthought to a Day-1 priority.

1. The “Day 3” Rule: Shifting Insurance to the Front of Escrow

In 2026, waiting for the final week of a 30-day escrow to secure insurance is a professional liability.

- The Problem: Traditional online quote declinations increased significantly recently, leaving buyers scrambling.

- The Move: Top agents now require buyers to submit an insurance application within the first 3 days of an accepted offer.

- The Goal: Identifying if a property is on an “Insurability Blacklist” before the buyer spends thousands on inspections and appraisals.

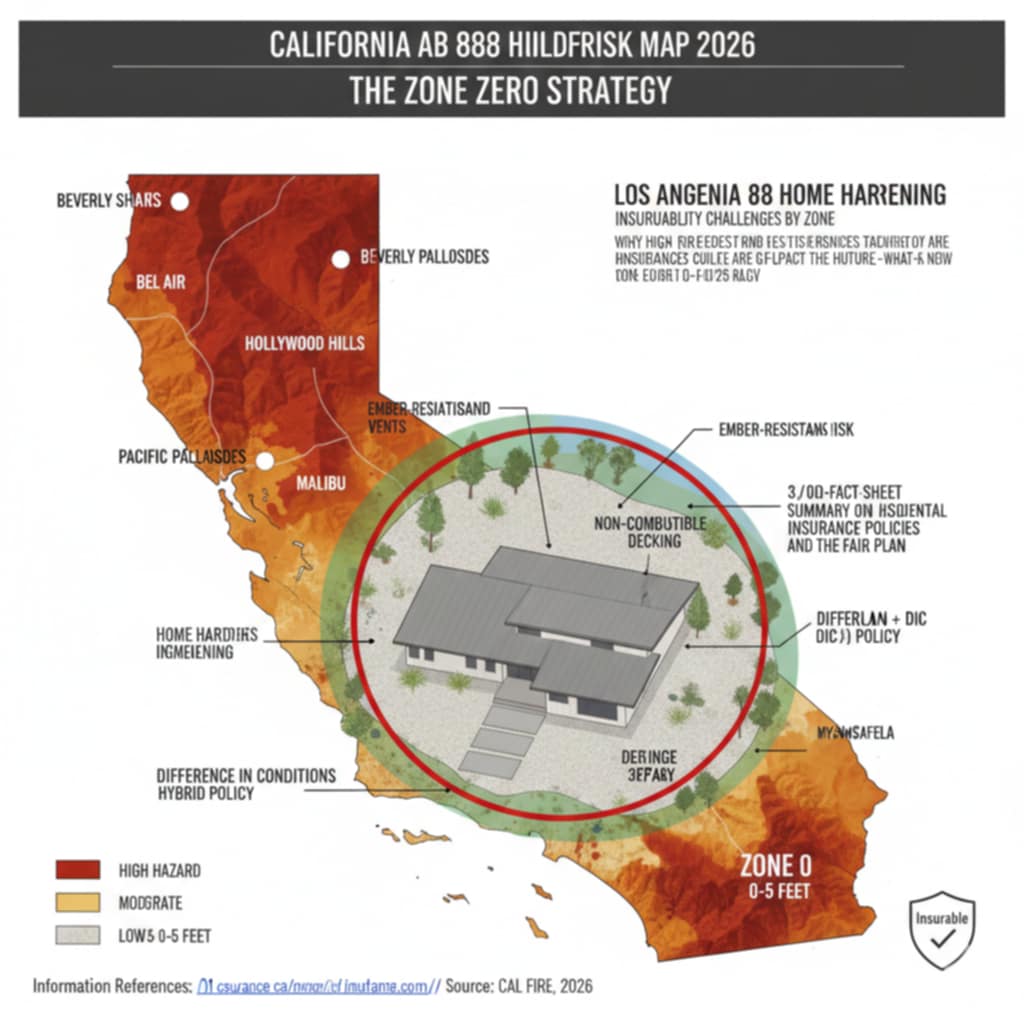

2. Mastering “Zone Zero” & AB 888 Compliance

California Assembly Bill 888 has shifted the responsibility of fire-hardening directly into the real estate transaction.

- The Requirement: Homes in high-fire hazard zones must establish a 5-foot “Zone Zero” ember-resistant zone around the structure. This includes removing mulch, wooden fences, and certain vegetation (MySafeLA).

- The Competitive Edge: By advising sellers to complete “home hardening” before listing, you aren’t just selling a house; you’re selling a “Certified Insurable Asset.”

3. The “FAIR Plan + DIC” Hybrid Strategy

When private carriers exit, the California FAIR Plan is the last resort.

- The Knowledge Gap: Many buyers walk away because they think the FAIR Plan is “bad coverage” since it only covers fire and smoke.

- The Solution: Educate your client on the “Difference in Conditions” (DIC) policy. This companion policy “wraps around” the FAIR Plan to provide liability, water damage, and theft coverage, essentially restoring the buyer to a standard HO-3 level of protection (California Dept of Insurance).

Summary: Turning a Crisis into a Competitive Advantage

The Insurance Exodus has created a massive coverage shortfall in Los Angeles. By mastering these strategies, you ensure your value is indispensable. In this environment, an agent who can navigate complex insurance bails, understand the legalities of AB 888, and properly structure a FAIR Plan/DIC hybrid policy is providing value that a digital portal like Zillow simply cannot match.

By mastering the “Insurance Deal-Killer,” you establish yourself as a specialized authority in the Southern California market—protecting your clients’ equity and ensuring your own commissions aren’t lost to the “Escrow Killer.